Click to Download Full PDF Here

The following is summary of a limited items regularly shared in CEIS’ Quarterly Loan Portfolio Quality Trends reporting for Client distribution.

CEIS enjoys a business relationship with approximately 100+ commercial lending Institutions, of which approximately ~two thirds being Community Banks. CEIS’ other Clients are larger specialty lenders, foreign banking offices, and other commercial lending organizations domestically and abroad.

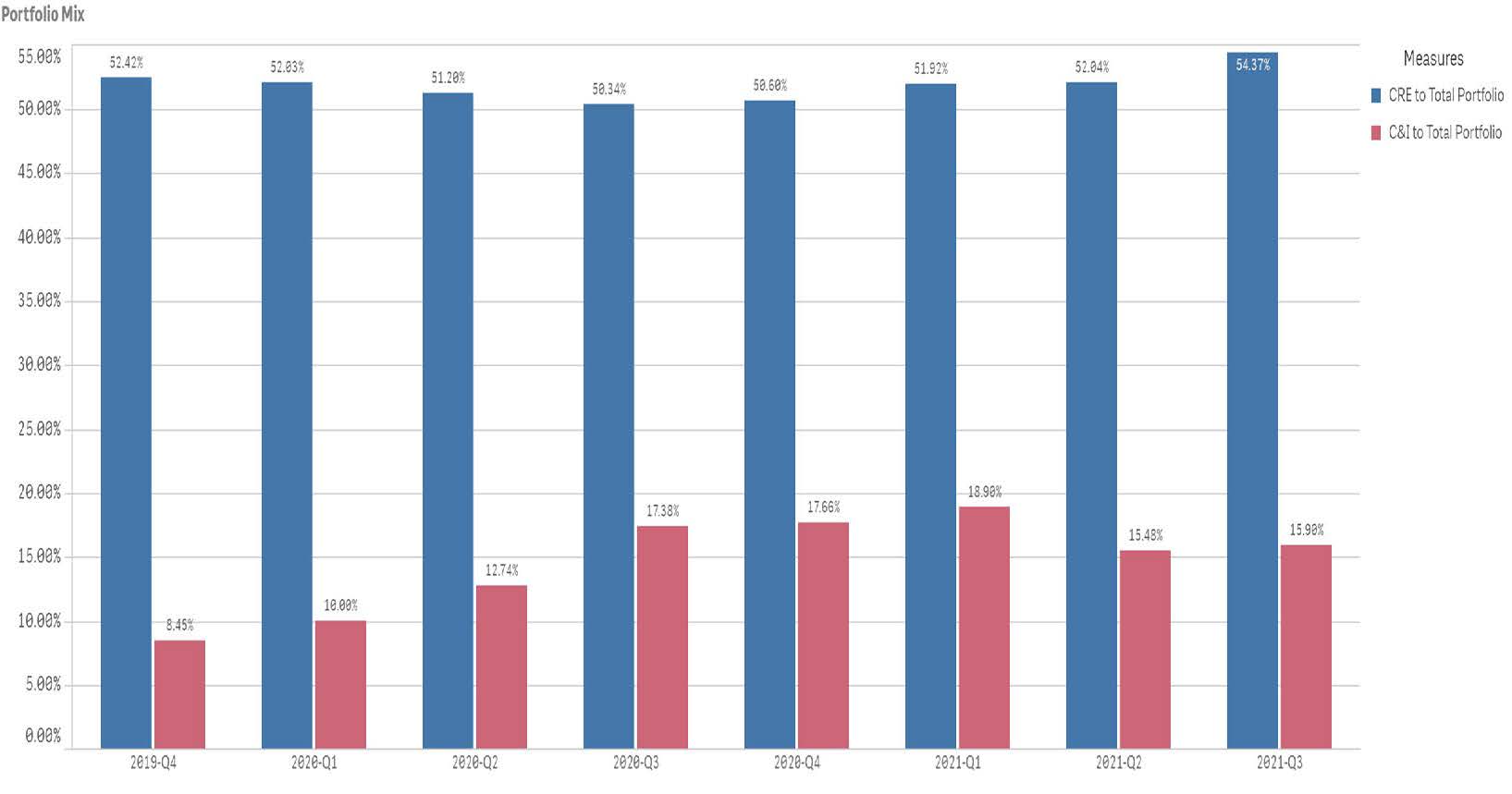

Portfolio Mix –CRE vs. C&I

CEIS’ Client’s portfolios are most heavily weighted in commercial real estate (CRE) representing on average just over 50% of total portfolio, followed by the commercial & industrial (C&I) segment at 15.9% of total portfolio on average of CEIS’ Client’s portfolios. The rise in C&I in 2020 through 1Q21 largely reflects PPP Activity, with declines in Q221 starting to reflect PPP loan forgiveness.

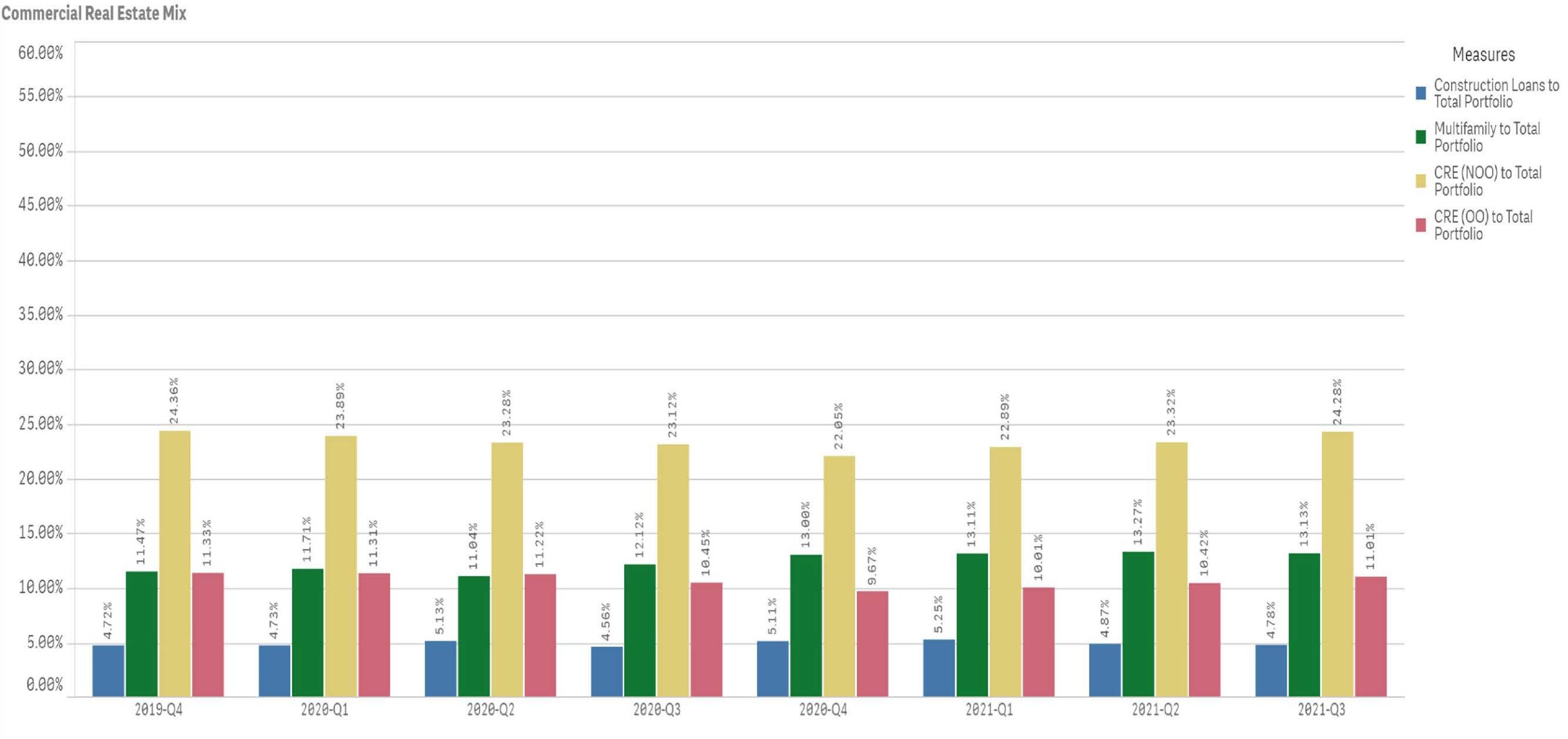

CRE Portfolio Mix

A more detailed look within CEIS’s Clients CRE portfolios shows that CRE (NOO) loans represent 24%, followed by multifamily at 13%, and then owner-occupied trailing at 11% of CRE. Construction has maintained an average of approximately ~5% of CRE portfolio throughout the reported quarters.

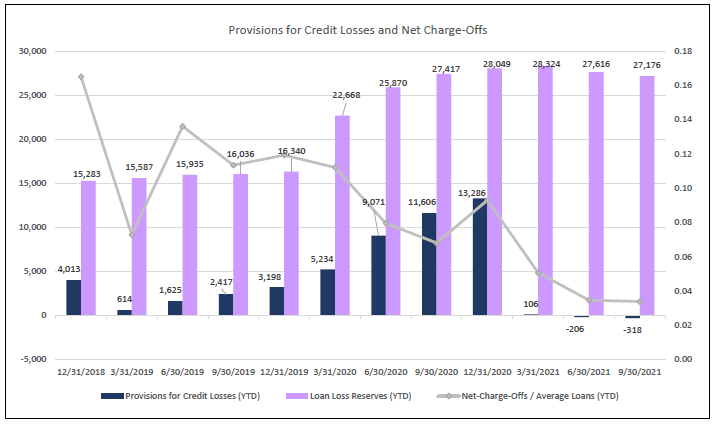

Provisions for Credit Losses, Reserves and Net Charge-Offs

Credit loss provisions for CEIS’ client base has dropped notably since FYE20, with the 3Q21 showing a modestly negative provision. Loan loss reserves for the group showed a slight decrease with net credit losses decreasing from 0.09% at FYE20 to 0.03% at 3Q21.

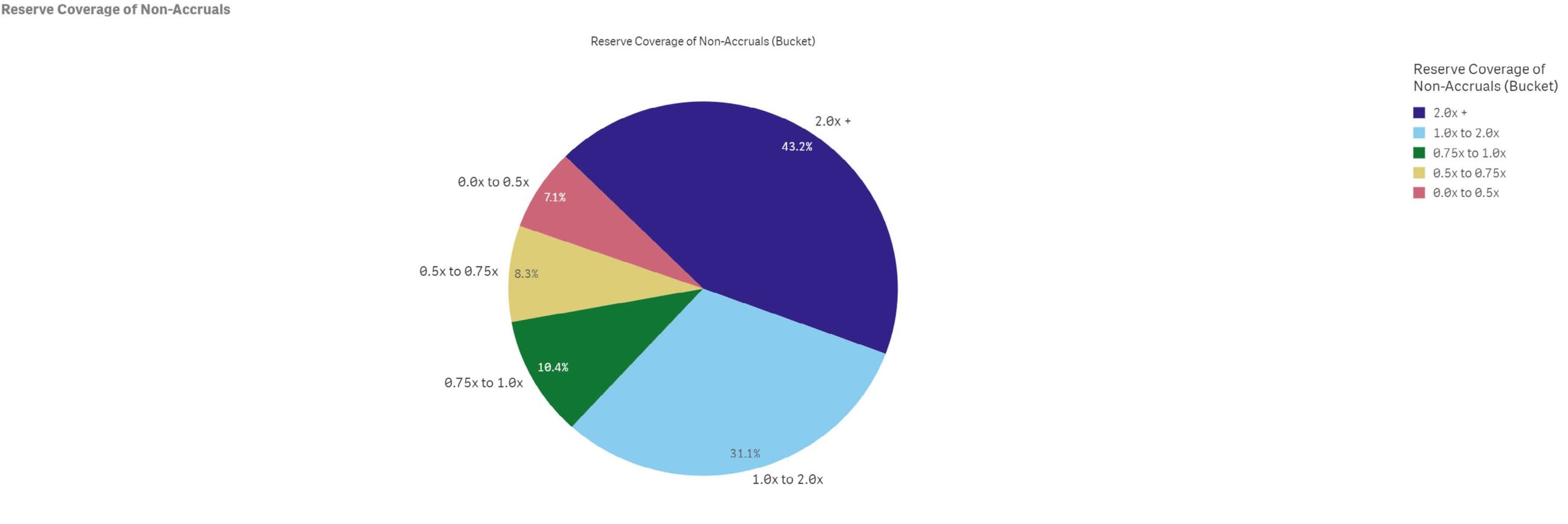

Reserve Coverage

LLR to Total Portfolio has increased in each period from 1.06% in 4Q19 to 1.24% in 2Q21

Loan Quality Indicators

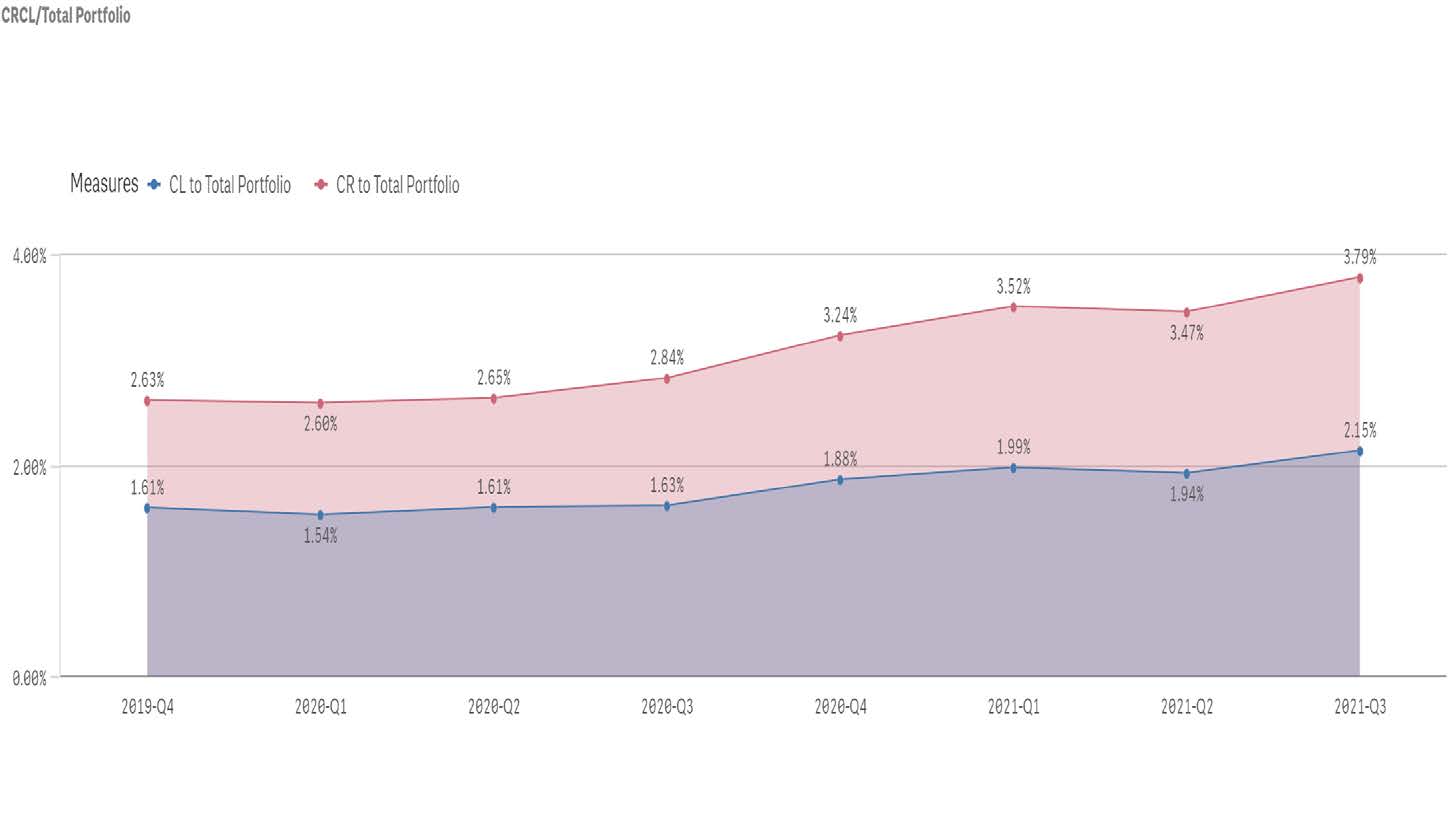

Criticized & Classified (“CrCl”)/ Total Portfolio

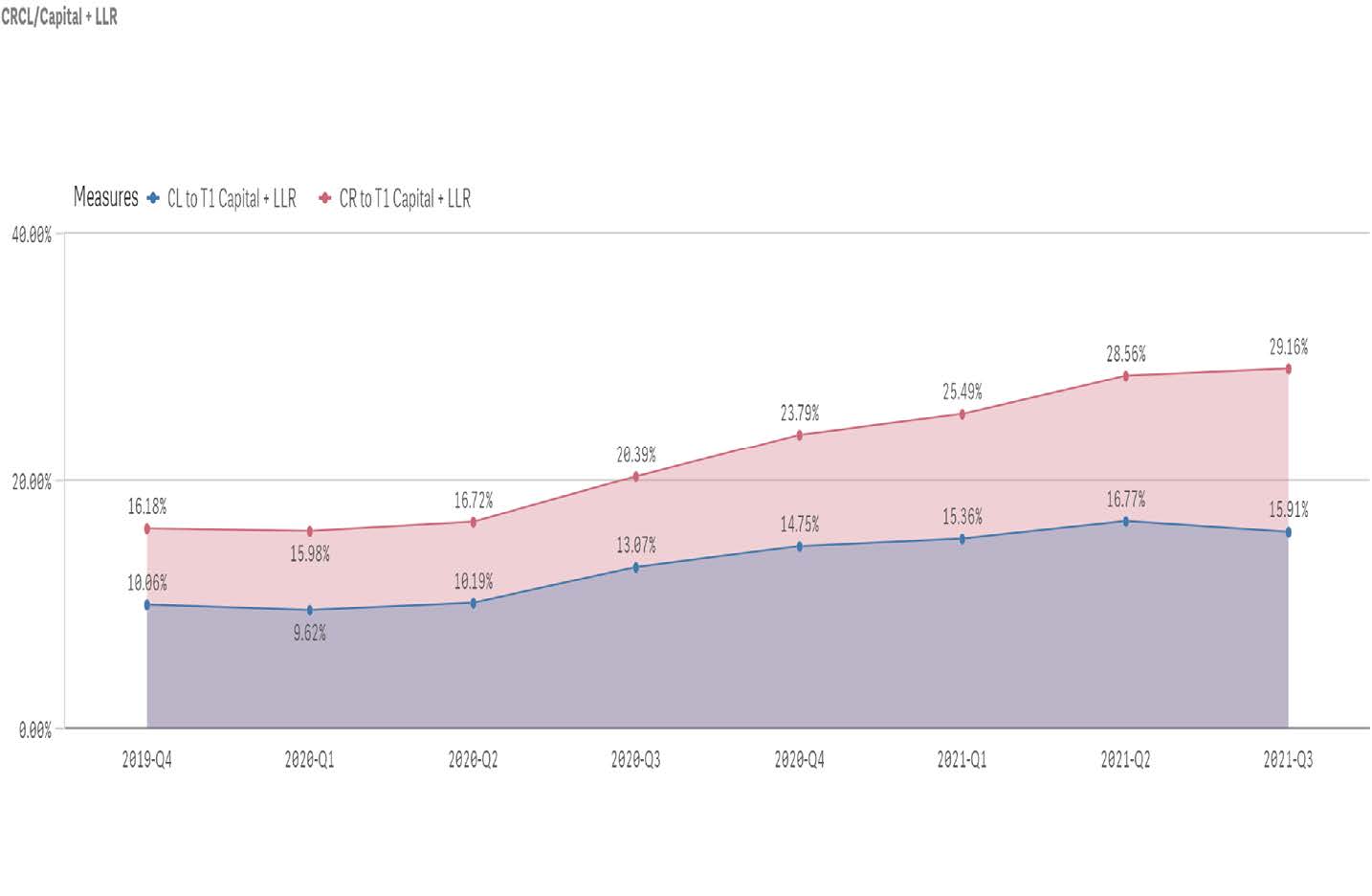

Criticized loans to Tier 1 capital + LLR has climbed to 29.16% for 3Q21, from 20.39% during 3Q20. The more critical ratio of classified loans to Tier 1 capital + LLR declined to 15.91% at 3Q21 from 16.77% at 2Q21, however, is still above the 13.07% reported one year earlier at 3Q20.

Evidenced adjacently, (SM, SS, D) loan levels were relatively unchanged from 4Q19 – 2Q20 with moderate increases beginning 3Q20 and continuing through 3Q21 at 3.79%.

Classified (SS, D,) loan levels have followed a similar trajectory as their related criticized assets with an increased variance from criticized assets beginning in 3Q20 and continuing through 3Q21 at 2.15%.

The increased variance reflects growth to SM due to COVID-19.

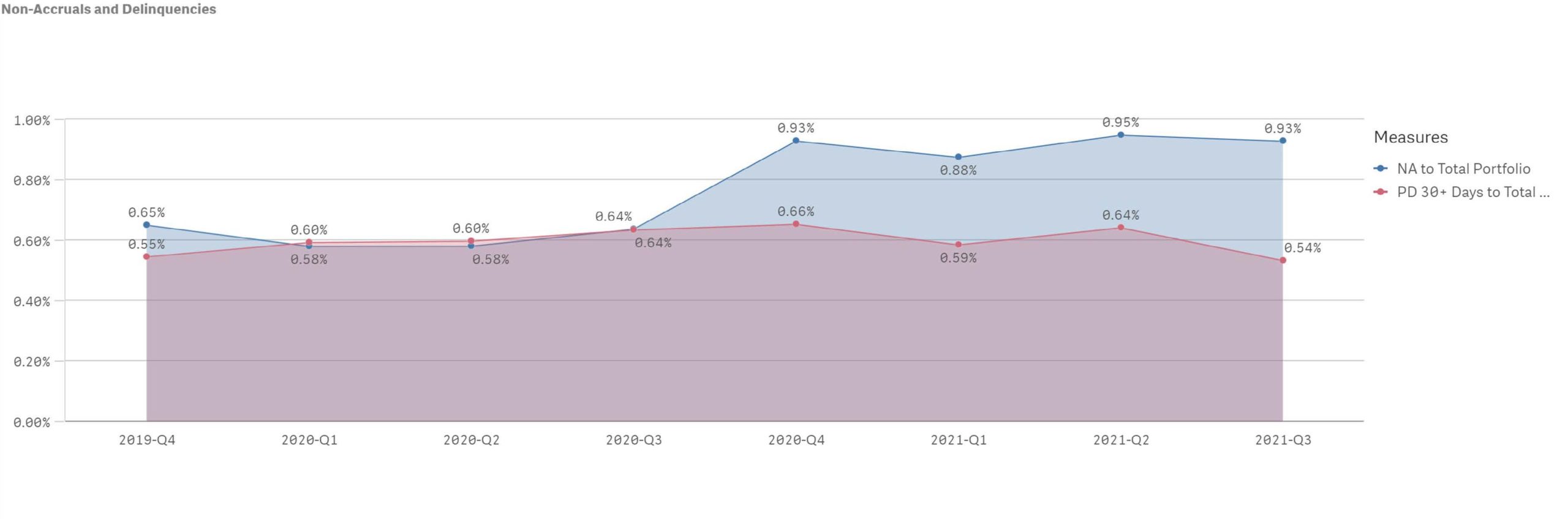

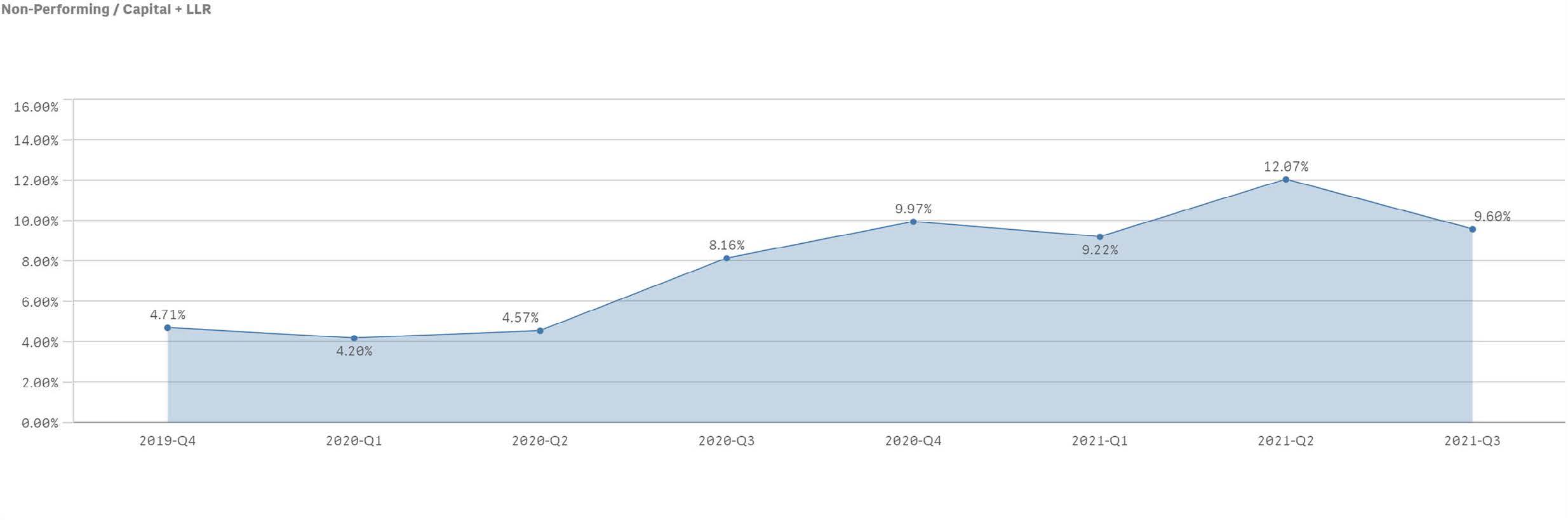

Non-Performing Loans

Grade Outlook –All Loans

The following are CEIS’ estimates of the six-month outlook for assigned Risk Ratings.

CEIS’ estimates of grade outlook have been trending upward since 2Q20 in that positive and stable estimates have increased notably since that time, while negative estimates plus those risk ratings assigned “insufficient data (ISD)” have declined. The trends reflect a pattern of confidence from continuing receipt of additional financial information from obligors.

The level of loans estimated to have a stable grade outlook has increased to 85.67% at 3Q21 from 81.32% during 2Q21, however, they still remain somewhat below the 91.78% that was reported 4Q19.

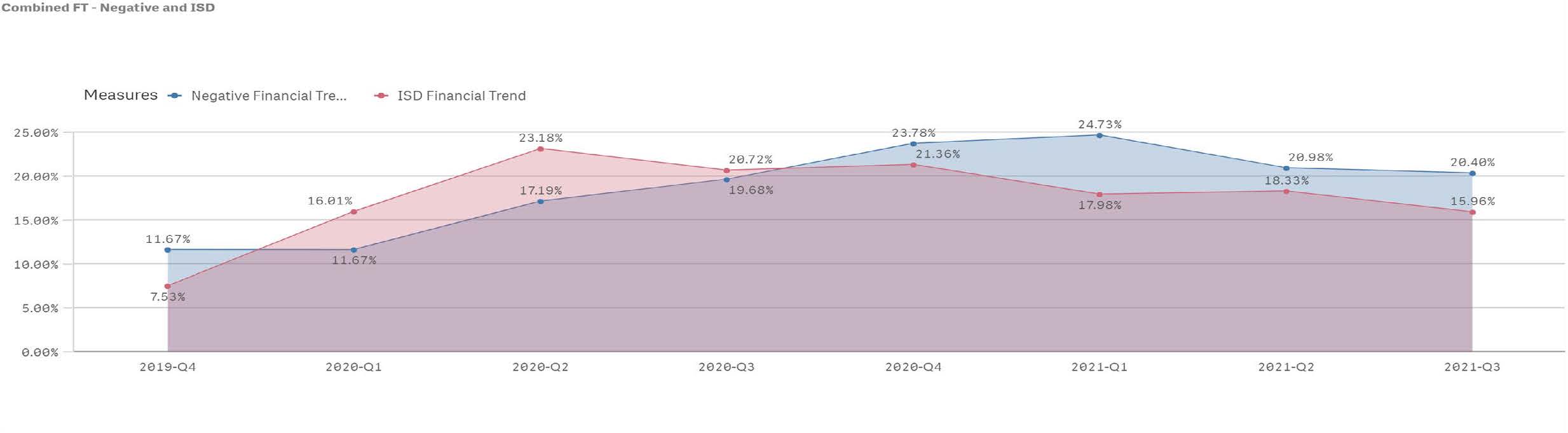

Financial Trend –All Loans

The following are the observations made regarding the financial trend of the borrowers reviewed.

Bank’s financial trend mix has changed notably since Q4 2019 with negative estimates plus those assigned “insufficient data” increased notably since that time. The level of loans assigned a negative financial trend continues to remain well above the low recorded of 11.67% during 4Q19.

Additionally, while loans assigned an ISD financial trend decreased from 18.33% at Q2 2021 to 15.96% at Q3 2021, this level also remains above the 7.53% reported for 4Q19.

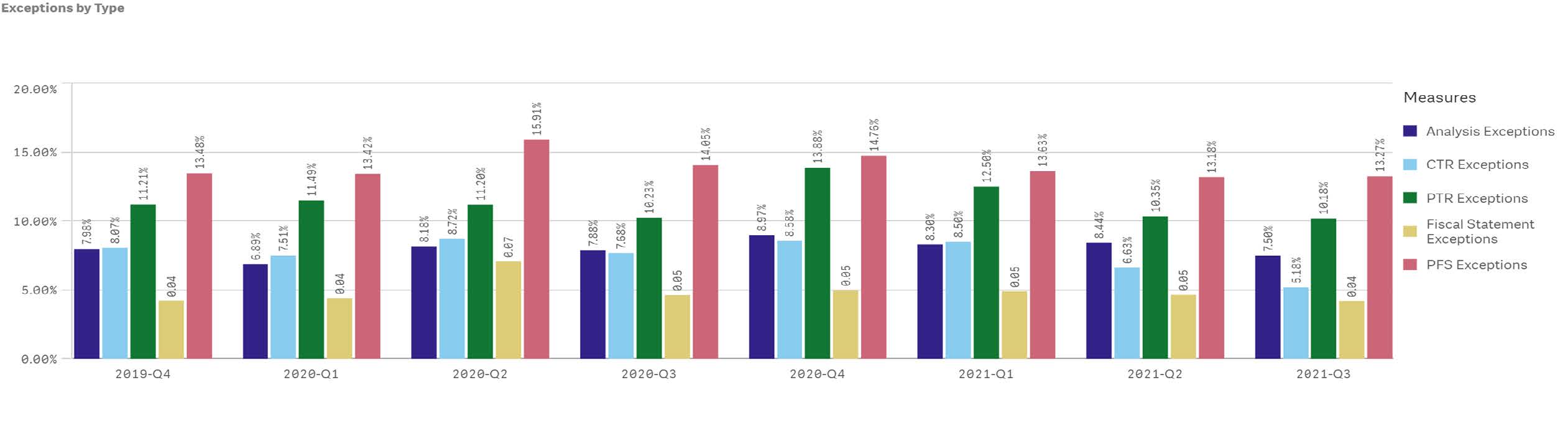

Technical Exceptions

Exceptions related to personal financial statement (PFS) and personal tax returns requirements (PTR) represent the highest exceptions by type at 13.27% and 10.18%, respectively, at Q3 2021.

Compared to the levels reported at Q2 2021 of 13.18% and 10.35%, respectively.

Combined technical exceptions at around ~30% have remained relatively unchanged since 2Q20.

New and Renewed Loans

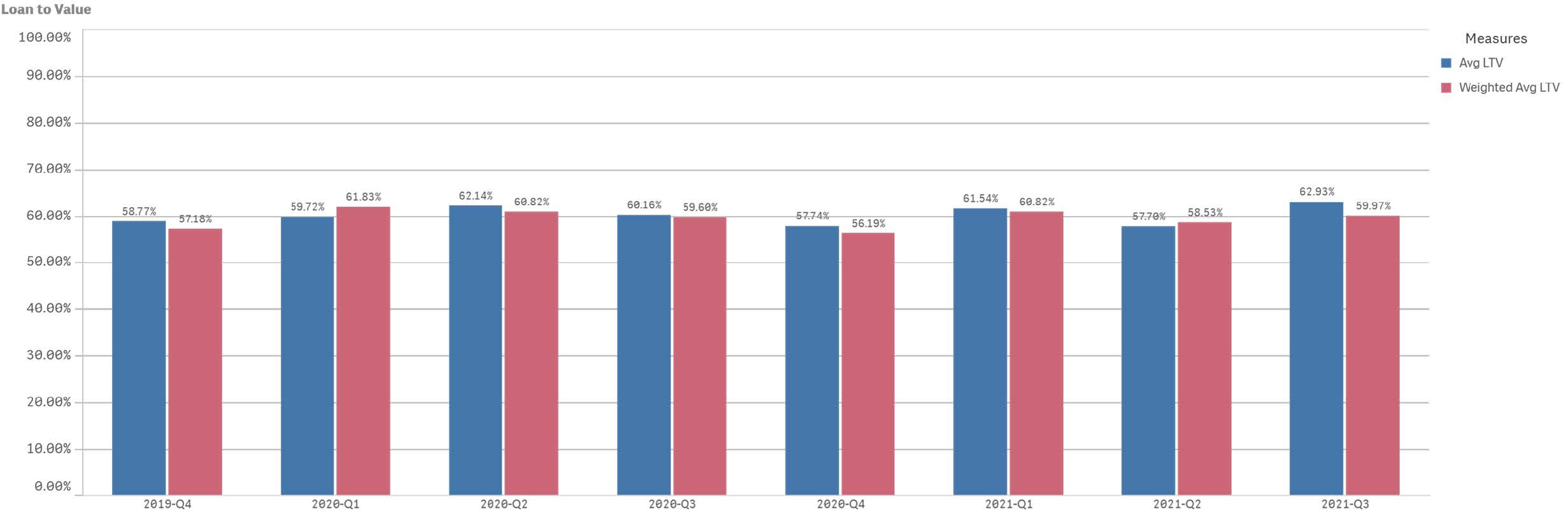

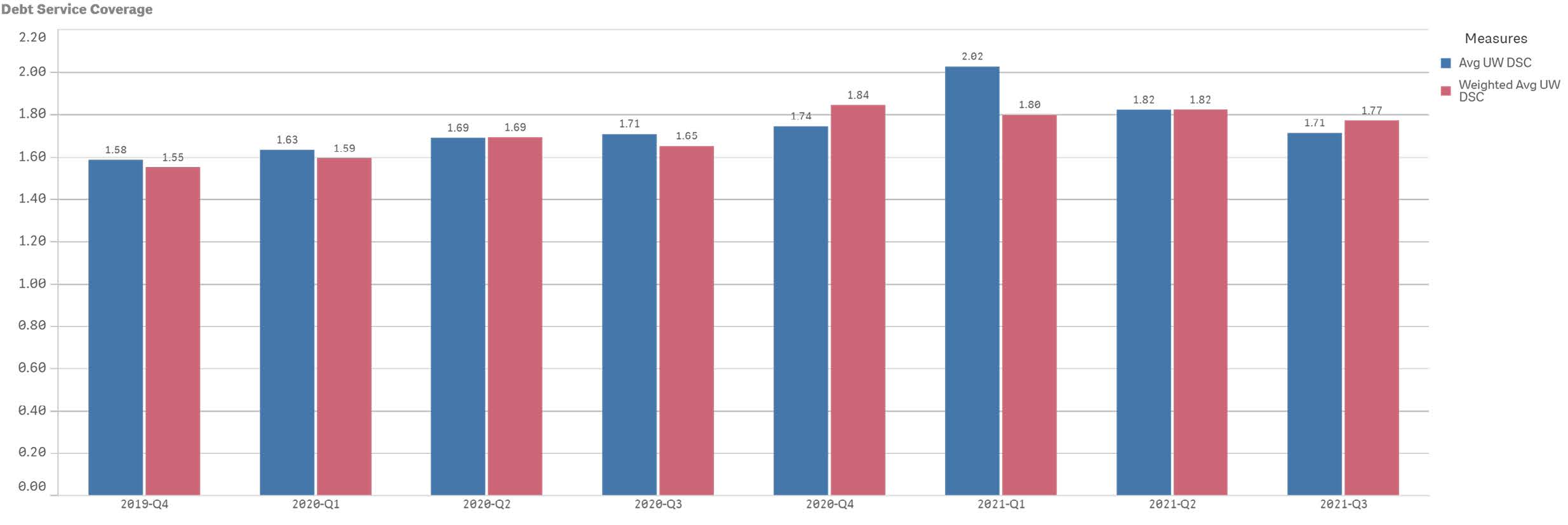

Loan to Value and Debt Service Coverage – CRE

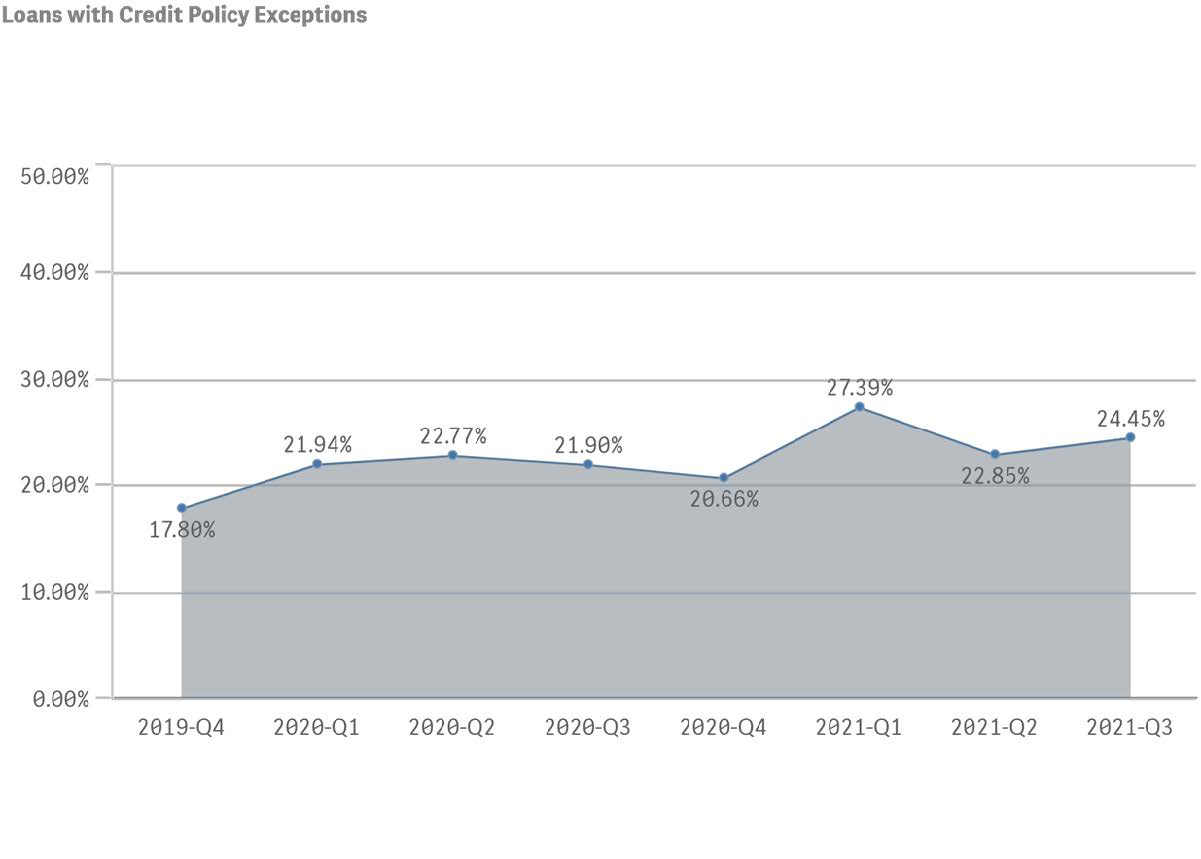

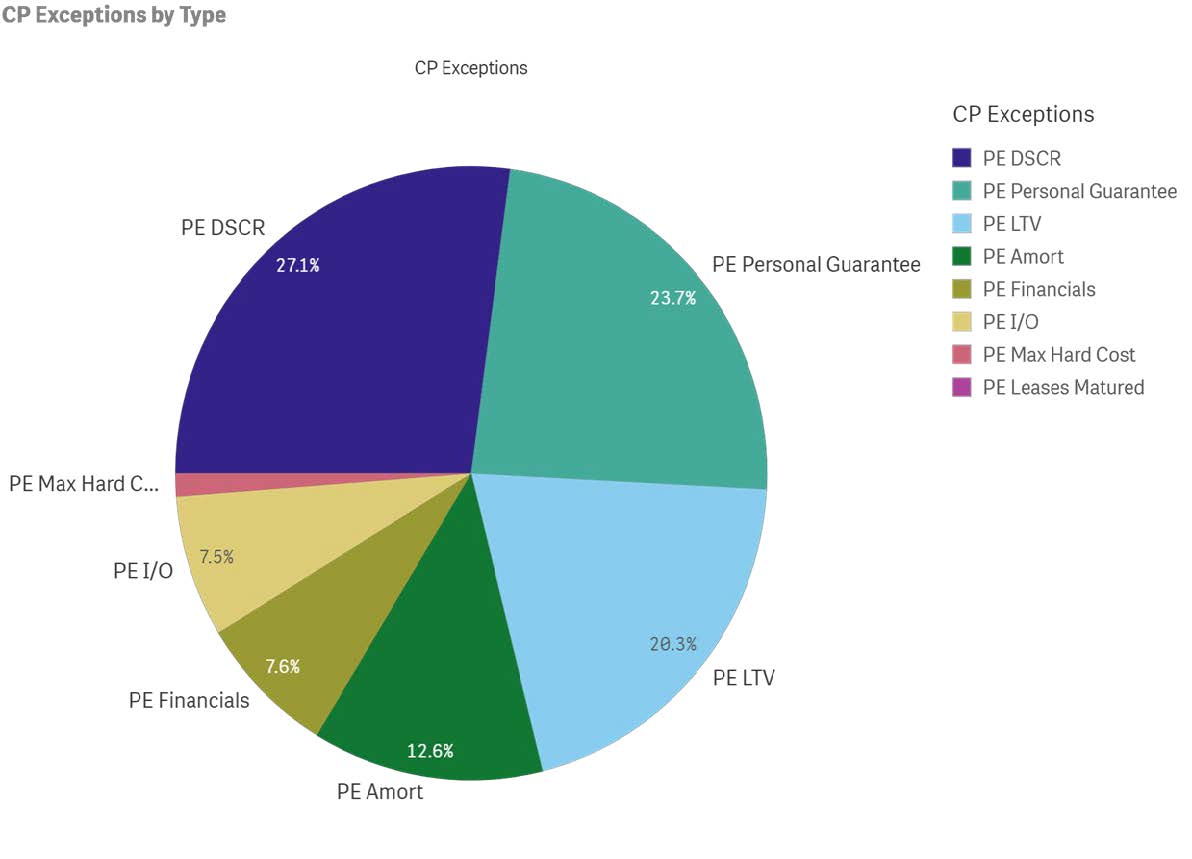

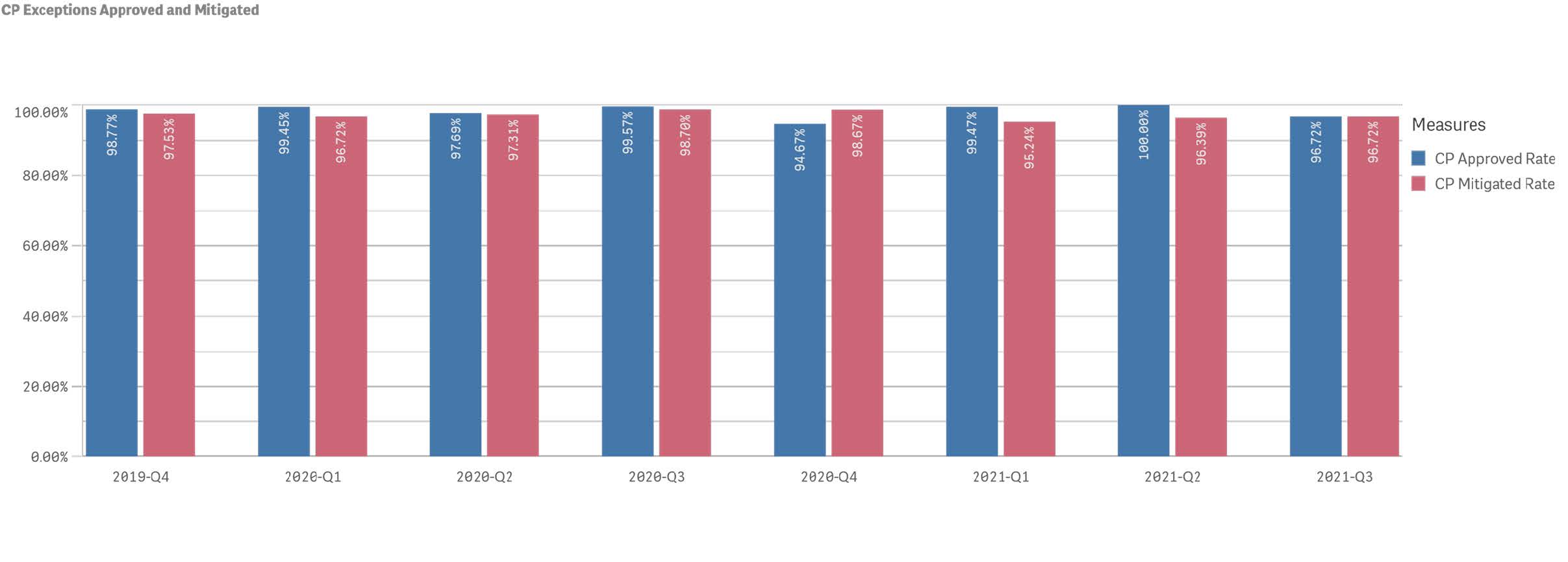

Credit Policy Exceptions

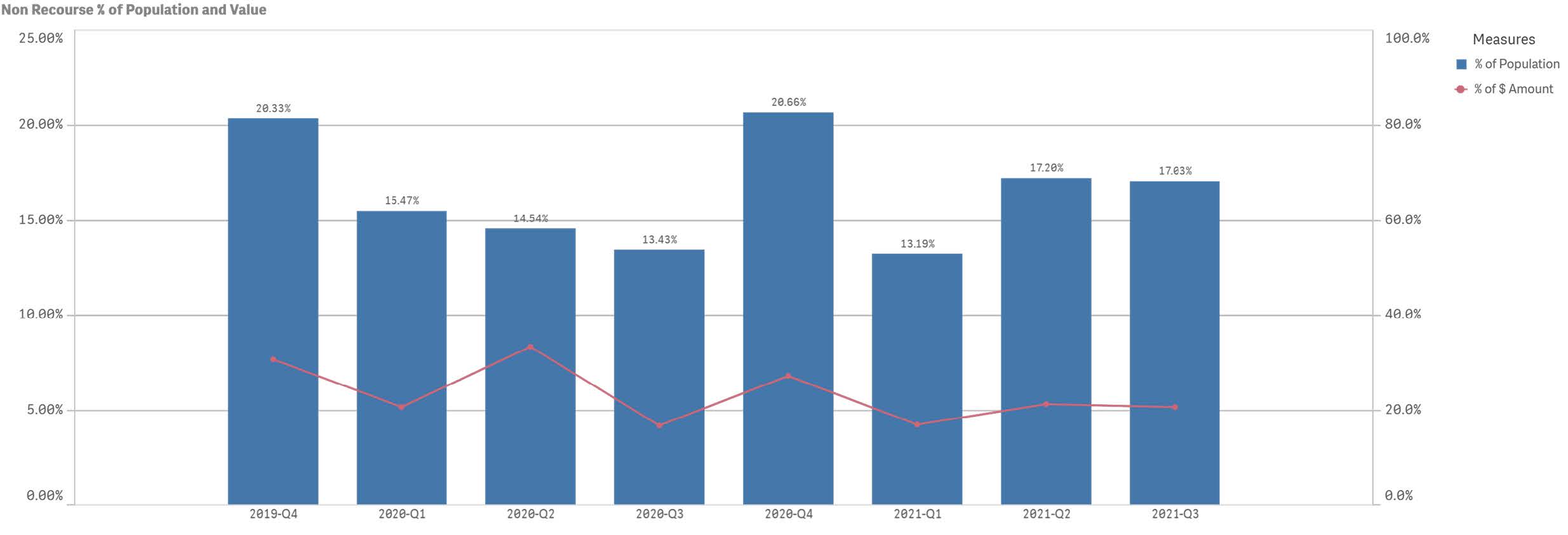

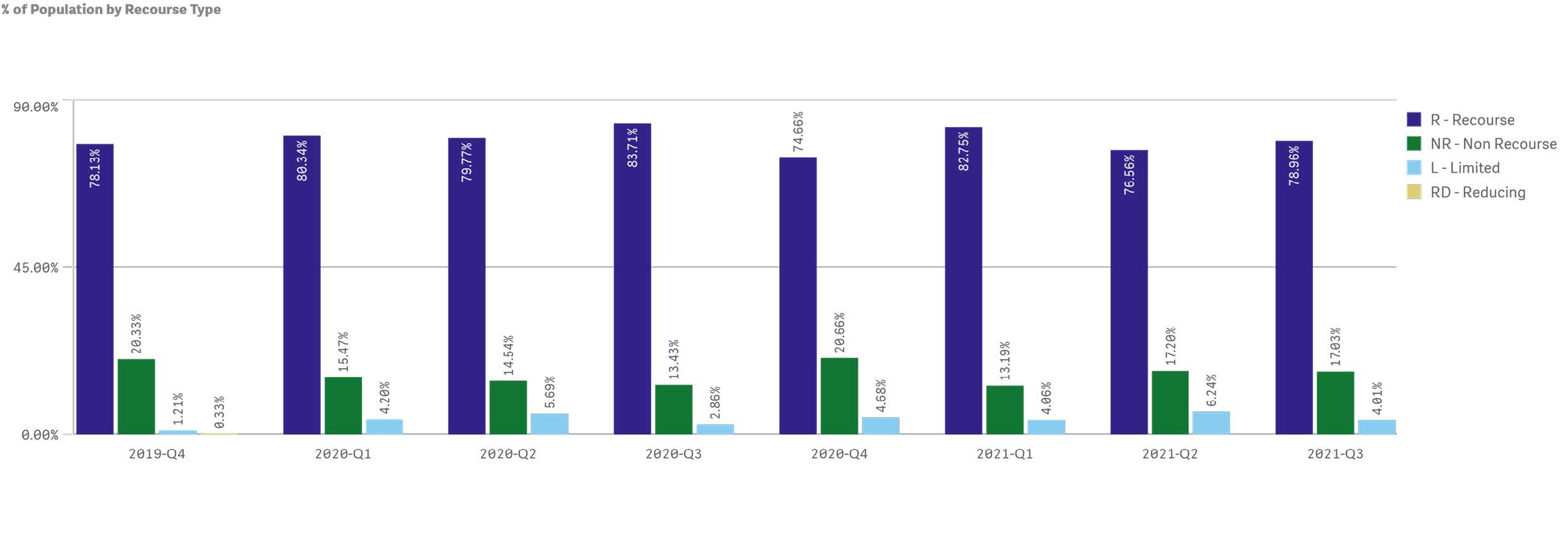

Non-Recourse

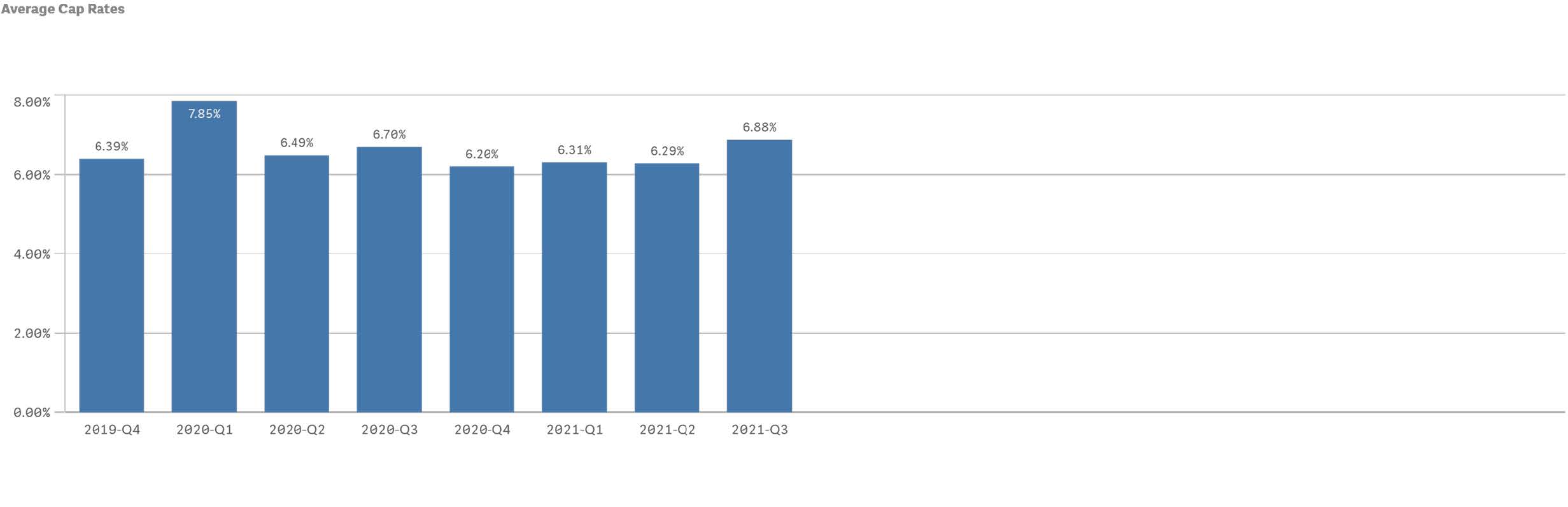

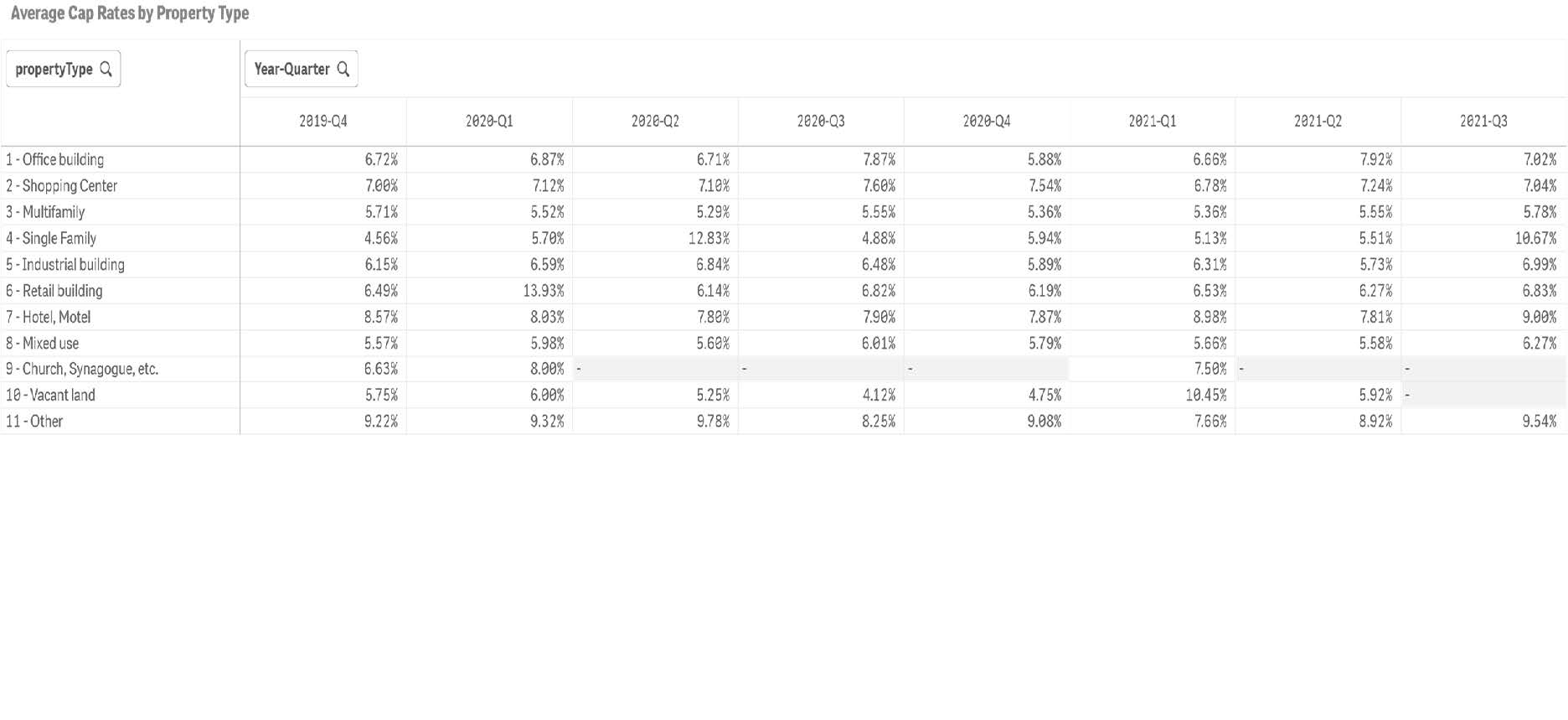

Cap Rates –CRE

Notable Concerns

- Manage and evaluate Credit Risk given changes in market conditions, termination of pandemic-related forbearance, uncertainties in the economy, and the lasting impacts of the COVID-19 pandemic.

- Focus on portfolios hard hit by the pandemic that may experience amplified impacts from changes in market conditions.

- Borrowers requesting prolonged accommodation may be a higher risk. Loan accommodation and other forbearance measures may obscure traditional measures for loan performance metrics.

- Attention to supply chain issues in client supply availability and logistics disruptions. Ongoing shortages of baseline materials combined with higher prices, longer shipping times and a lack of workers continue to impact businesses.

- Emphasis on Portfolio Management – track and review borrower and guarantor financial information on a prompt basis to assist in timely determination of appropriates and covenant compliance calculations, in relation to risk management and protection of rights.

- More emphasis placed around timely and ongoing loan reviews with expectations that Banks increase the frequency of individual loan reviews based on severity of risk. Quarterly or monthly

reviews for higher risk transactions may be appropriate. - Risk Ratings – document the bank’s understanding of the key risks of each individual borrower, considering financial performance pre-COVID-19, the impact of COVID-19 both short term and long term, relief/stimulus provided during the pandemic, repayment ability, collateral, and industry considerations. Banks should be in close contact with their largest borrowers and those with higher risk loans.

- Stress Testing is recommended on both a loan and portfolio basis. The transactional to portfolio level in analysis is most beneficial in identifying weaknesses on a borrower-by- borrower basis as well in segments. A pandemic stress test analysis that segregates the NAICS code so Banks can see which industries are potential problem segments is also recommended.

![]()

CEIS Review is the market leading Commercial Loan Portfolio consulting firm established in 1989 by Bankers.

Loan Review, Portfolio Stress Testing, Reserve Methodology, Portfolio Acquisition Review (DD), Leveraged Lending, Loan Policy & Process Review, Customized Loan and Credit Seminars, and other customized engagements.

(888) 967-7380

[email protected]

www.ceisreview.com

[email protected]