How to Identify a Leveraged Loan in your Portfolio – The CEIS Quarterly Newsletter – Volume 4, Issue 2

Select here: The CEIS Review Quarterly – Volume 4, Issue 2 – 2018

New York, May 16, 2018 — CEIS Review Inc. is a Commercial Loan Portfolio Consulting firm serving the needs of Commercial Lending Institutions. In this issue of our newsletter, we discuss results of the Fed’s survey on bank lending practices, and how to identify a leveraged loan in your portfolio.

ON MY MIND…CEIS’ President, Joe Hill, shares his thoughts

In light of the Fed’s recent report which noted a decline in underwriting standards and increased appetite for risk (a report summary can be found on page 2), we’ve been thinking about the importance of safeguarding resilience in your portfolio in preparation for a potential downturn, small or large. On this note, we must stress that although the current environment is hospitable, that likely will not last forever. Looking forward, we always seek to keep our finger on the pulse of regulators’ concerns, as their main objective is to safeguard against any potential vulnerabilities that may emerge. Likewise, any major problems that do emerge will ultimately affect the way that banks are regulated.

The economic environment today is robust and very similar to that of a decade ago (1), so it’s important to look not to what is going well but what may present challenges in future. Regulators have recently observed elevated risk in two areas: asset valuations and business leverage. Asset valuations remain at a historical high, with prices rising for multifamily as well as commercial real estate, all while capitalization rates sit at historical lows. Nonbank business leverage is also at historical highs; debt-to-income ratios are above historical averages, and sub-investment grade firms are showing especially elevated net leverage ratios.

Appetite for risk is not a bad thing, given our industry (within the limits of your Institution’s risk appetite framework) but it is best practice to balance that out with comprehensive – not compulsory – stress testing to maintain sufficient insight into your portfolio. As a loan review firm, we are adamant about the importance of maintaining a healthy and prosperous portfolio because ultimately, we are dedicated to our Client’s success and growth.

Joseph J. Hill President & CEO

(1) https://www.federalreserve.gov/newsevents/speech/brainard20180419a.htm

Fed Loan Officer Opinion Survey: Summary

Each quarter, the Fed issues a survey to Senior Loan Officers to take the temperature on banks’ lending practices, including key factors like changes in loan standards or terms and observed loan demand (1). Our focus in this summary is on data from the 72 responses received from U.S. banks, and their reported observations in lending to businesses.

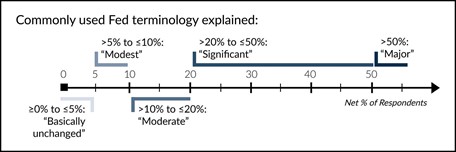

Please see a chart below which helps to explain the mathematical values behind terminology used throughout:

COMMERCIAL & INDUSTRIAL LOANS

Standards and terms for Commercial & Industrial loans were generally eased for large and middle-market institutions, but remained unchanged for small institutions. All banks who reported eased C&I underwriting in 1Q 2018 cited increased competition from other lenders as a reason. Other reasons for eased standards or terms in C&I were: increased risk tolerance, a more favorable economic outlook, reduced concerns related to government regulation (namely – legislation, supervisory actions, and accounting standards), and a general betterment of problems within the industry.

Weaker demand was reported by a modest net percent of large and middle- market firms over 1Q 2018. Banks in this group felt that declining demand was caused by customers shifting their borrowing to other sources of credit, as well as an increase in customers’ internally generated funds. Regarding profitability, a significant fraction of large and middle-market banks observed a narrowing of loan rate spreads, while a moderate fraction of small banks observed narrowed loan rate spreads.

COMMERCIAL REAL ESTATE (CRE) LOANS

Standards and terms were reported as tightening for Multifamily properties by a modest net percentage of banks. Nonfarm Nonresidential standards, conversely, were reported as eased by a modest net percentage of banks. Construction and Land Development loan standards were generally unchanged. Increases in maximum loan size and spread of loan rates over cost of funds were the specific changes that contributed to eased underwriting, and these occurred across all three major categories – Construction & Land Development, Nonfarm Nonresidential, and Multifamily. However, Debt Service Coverage ratios changed very little on all categories.

Regarding demand across the three main CRE categories, there was a stark divergence among responses. Stronger demand was reported by a modest share of banks; conversely, weaker demand was also reported by a modest net share. Interestingly, among both groups, answers from small and large banks were similar. Those who experienced strengthened demand credited increases in customers’ acquisition or development of property as important factors. Those who reported decreased demand attributed just the opposite: decreases in customers’ acquisition or development of properties and shifts of customer borrowing to other banks/nonbank sources.

TRENDS

The Fed has observed a reversal of CRE underwriting trends: while banks reported a tightening of most lending policies throughout 2016, a net easing was observed through 2017 to present. A major fraction of banks cited aggressive competition from banks and nonbank lenders contributing to eased credit policies. Additional important contributing factors in easing standards and terms reported by a significant net percentage of banks were increased tolerance for risk, current capitalization rates, and more favorable outlooks in the industry (namely – CRE property prices, vacancy rates, and other fundamentals).

Across both C&I and CRE lending, we see a common sentiment, which is that banks are now more commonly easing underwriting standards. The main reason for this, competition among banks and nonbank lenders, is a common refrain; however, we are now seeing an increased appetite for risk. In Warren Buffett’s 2017 annual letter to shareholders, he addressed this recent intensification in risk appetite (2). Addressing the stark uptick in acquisitions, Mr. Buffett expresses that Wall Street analysts or board members suggesting that an acquisition be considered is akin to “telling your ripening teenager to be sure to have a normal sex life.” All jokes aside, this is an interesting trend that has been presented and we are curious to see what the future holds.

https://www.federalreserve.gov/data/sloos/sloos-201804.htm

http://www.berkshirehathaway.com/letters/2017ltr.pdf

How to Identify a Leveraged Loan in Your Portfolio: A Brief Overview

I think we can all agree that Risk Management is a chief objective in maintaining a healthy portfolio. Regulatory guidance (1) states that in a broad sense, the main risks connected to leveraged lending are “credit, interest rate, liquidity, price, foreign exchange, transaction, compliance, strategic, and reputation. These categories are not mutually exclusive; any product or service may expose a bank to multiple risks.” Given that in lending, many decisions require dynamic assessment of the situation, we at CEIS seek to provide some clear indicators we’ve observed in leveraged loans. In this article we elaborate on four multifaceted ways of identifying a leveraged loan: (a) purpose, (b) ratios, (c) debt markets, and (d) industry. The Interagency Guidance on Leveraged Lending (2) (the “Guidance”), requires that banks which are engaged in leveraged lending adopt policies that include criteria to define leveraged lending that are appropriate to the institution. The Guidance further states that numerous definitions of leveraged lending exist throughout the financial services industry and commonly contain some combination of the following four elements.

PURPOSE

A loan may be considered to be leveraged wherever a loan’s purpose is for buyouts, acquisitions, or capital distributions. Buyouts funded by loans are, by definition, leveraged buyouts. Likewise, acquisition finance transactions are also, by definition, leveraged buyouts (LBOs) when all or part of an acquisition is funded by a material amount of debt. In these transactions, the source of repayment is typically cash flow from operations, refinancing of debt, an Initial Public Offering (“IPO”), or sale of the company.

Debt financed capital distributions are when cash is disbursed to stakeholders in a business in order to monetize a portion of the value owned, but without selling their ownership interests. These transactions are considered leveraged because the business’ value is being leveraged to raise capital.

RATIOS

Leverage ratios are used to put in perspective how much debt is created as a result of the above transactions. Generally speaking, the Guidance indicates that Total Leverage >6.0X raises concerns for most industries.

The Total Debt to Earnings Before Interest, Depreciation and Amortization (Debt to EBITDA) ratio is considered an industry standard in determining a borrower’s ability to pay off its debt, or responsibly take on additional debt in order to grow. Broadly speaking, ratios higher than 4.0X are considered leveraged.

https://www.occ.treas.gov/publications/publications-by-type/comptrollers-handbook/leveraged- lending/pub-ch-leveraged-lending.pdf

https://www.federalreserve.gov/supervisionreg/srletters/sr1303a1.pdf

Likewise, Senior Debt to EBITDA should also be considered where relevant. Senior debt is important to consider as it must be repaid first in a scenario where the borrower goes out of business. For determining leveraged loans specifically, regulators consider Senior Debt to EBITDA ratios greater than 3.0X to be leveraged.

We should note that certain industries may have different ratio thresholds for Debt to EBITDA and Senior Debt to EBITDA, or other defined levels appropriate to the industry or sector (see Industry below). It’s also important to note that the Guidance does not allow the netting of cash from debt in the above ratio calculations. The Guidance also stipulates that you must include all unused commitments as though funded in the debt calculation including delayed draw term loans, lines of credit, and accordion features.

DEBT MARKETS

A borrower recognized in the debt markets as a highly leveraged firm, which is characterized by a high debt-to-net-worth ratio, is a factor for consideration when determining leveraged loan status. Know your customer: good bankers are characterized by their shrewd use of discretion and common sense in making decisions. So logically, it’s important to remember the obvious markers of leveraged transactions and to consider if the borrower can be recognized in debt markets as leveraged. Similarly, look for transactions where the borrower’s post-financing leverage, as measured by its leverage ratios significantly exceeds industry norms or historical levels as described in specifics above.

INDUSTRY

The credit ratios described above are intended as high-level principles and do vary by industry, requiring an informed judgment call. How the borrower is viewed within the industry, and stability of each industry within the current environment will always be a key matter of significance. Credit ratios that significantly exceed industry norms or historical levels are factors for consideration when determining leveraged loan status.

WHAT & WHEN

You know what to look for, the only question is when these characteristics are applicable. The Guidance indicates that the designation of leveraged loan status is typically determined at the time of the loan’s origination, and can also be determined when a loan is modified, extended, or refinanced – basically, any time there is a material modification to the structure of the loan. Below we outline the two specific loan types that fall outside the scope of leveraged lending guidance.

“Fallen angels”, or loans that were initially non-leveraged and healthy but have subsequently deteriorated to a point where the ratios technically fall in the leveraged range, should be considered as simply problem loans until they are modified, extended, or refinanced, at which time the loan should be looked at and reevaluated.

Asset-based loans also fall outside the scope of leveraged lending guidance, except in cases where they are “part of the entire debt structure of a leveraged obligor.” For asset-based loans to be excluded from leveraged loan consideration, the asset- based financing must represent the vast majority of debt within the borrower’s capital structure. Furthermore, the distinction of traditional asset-based lending carries with it tight controls and monitoring as is, as well as being secured by specific assets and governed by a borrowing formula which is determined based on the specific assets unique to each situation.

Related Links

- Bank Deregulation Bill Clears Congress

- Federal Reserve issues Federal Open Market Committee Statement

- New York Stock Exchange to Have First Female Leader in 226-Year History

- FDIC-Insured Institutions Report $56 Billion in Net Income in First Quarter 2018, Community Bank Net Income Increases to $6.1 Billion

- Economists See Fed Raising Rates in June, Then September

- PayPal Pays Up to Get Into Stores

- Interactive Game: Do you have what it takes to run an American Mall?

About CEIS Review

CEIS Review, Inc. is an independently owned financial consulting firm founded in 1989 by proven commercial lenders who specialize in commercial loan portfolios.

Services include:

Loan Review Programs

Portfolio Acquisition review (Due Diligence)

Structured Finance Review (Leveraged Lending)

Commercial Portfolio Stress Testing

ALLL Methodology Validation or Advisement

Credit Risk Management Process Review

Training Workshops

For information, email Justin J. Hill at [email protected]

Engaged ▪ Proven ▪ Trusted