Recent Trends in New and Renewed Underwriting Standards -The CEIS Quarterly Newsletter Issue 3, Volume 3

To view as a PDF select here.

New York, August 10, 2017 — CEIS Review Inc., a financial services consulting firm serving the needs of commercial and savings banks, has released its survey of loan quality trends as observed from reviews of its client base.

ON MY MIND…CEIS’ President, Joe Hill, shares his thoughts

Regulators have been keeping a very close eye on the quality of the underwriting that Banks are putting onto their books for the past couple of years. Specific concerns were that new/renewed activity was heading for lower quality standards as Banks strived to beat out the competition, and then as the Banks grow that they have the proper risk management framework in place to appropriately manage their portfolios.

Regulators have been keeping a very close eye on the quality of the underwriting that Banks are putting onto their books for the past couple of years. Specific concerns were that new/renewed activity was heading for lower quality standards as Banks strived to beat out the competition, and then as the Banks grow that they have the proper risk management framework in place to appropriately manage their portfolios.

CEIS looks at over 130 client institutions throughout the year, and as such, we accumulate data that enables us to perform analysis on portfolio quality metrics on a periodic basis. In regards to new/renewed loan activity, there are a few metrics that I would like to share.

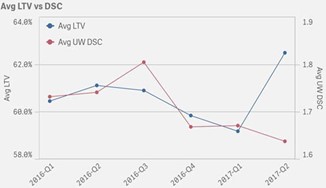

The analysis has shown that the quality of the underwriting on new or renewed transactions that CEIS has reviewed over the prior few quarters have generally exhibited reasonable ranges for both Loan-to-Value (LTV), as well as Debt Service Coverage (DSC) ratios. Loan to Values have averaged 60.39%, with Debt Service Coverage Ratios averaging 1.73x.

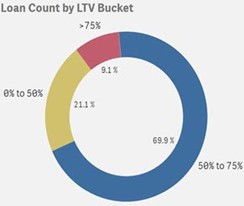

Further analysis shows that of the 3,120 new or renewed transactions included in this sampling pool, approximately 70% of the transactions exhibited the Loan-to-Values between 50% and 75% with~21% between 0% and 50% and ~9% above 75%. This shows that while the averages are overall conservative, within the sampling there is a fairly broad range of the specific LTV values which contribute to the overall average of 60.39% LTV average value.

In the market, this finding appears converse to the public consensus of loan quality deteriorating; however, there is a lag in CEIS’ data and the data does not necessarily reflect what CEIS has observed as a gradually increased risk in some portfolios by way of concentrations and/or introduction of loan types not previously in the portfolio mix as well as a level of new loans in many portfolios being untested in adversity.

In the market, this finding appears converse to the public consensus of loan quality deteriorating; however, there is a lag in CEIS’ data and the data does not necessarily reflect what CEIS has observed as a gradually increased risk in some portfolios by way of concentrations and/or introduction of loan types not previously in the portfolio mix as well as a level of new loans in many portfolios being untested in adversity.

According to the Fed, “July survey results indicated that, on balance, demand for commercial and industrial (C&I) loans weakened over the second quarter of 2017 while banks left their standards on C&I loans basically unchanged.”

So a few things appear evident: (a) demand remains constant for CRE while C&I has slowed, (b) competition continues and shows itself in pricing and terms, (c) CEIS’ stats on loan quality are thus far only showing modest shifts in loan quality.

Where we are going to land after changes to Dodd-Frank and other regulatory policies and practices is unknown at this point, but as long as lenders remain diligent in performing a thorough analysis of our borrowers, underwrite new activity appropriately, manage those relationships with attention and objectivity, ensure our institutions are looking at the portfolio as a whole from a risk perspective while anticipating changes (i.e. stress testing), we have done a prudent job and contributed our full to the Banking Community.

Joseph J. Hill President & CEO

CONSTRUCTION LENDING RAISING THE BAR

There is no denying that Commercial Real Estate (CRE) Construction activity is all around us. Whether you live in a metropolis such as NYC or in a more suburban or rural setting, you likely pass by at least a few projects on your daily commute: Perhaps your institution is even financing a few of those. Today’s commercial lending environment has seen many regulatory changes, some of which specifically pertain to Construction Lending.

With the active Construction Lending market in place, there is an opportunity for institutions to meet their customers’ needs, generate additional income, diversify an institution’s portfolio, and generally grow. With all of the possible positives, remember that if engaged in incorrectly, a Construction Lending portfolio can become a great burden for an inexperienced institution to handle, even resulting in an institution’s failure. To avoid such problems, we thought it might be useful to revisit some principles of a sound Construction Lending Program.

The areas that should be looked at to gain an assessment of your Construction Program are regulatory – an institution’s current standing, and its ability to maintain compliance with guidelines in this specific type of lending; expertise – in-house as well as vendors and potential participating parties; and institutional risk tolerance – establishing acceptable levels of risk, then determining ways to track those risk tolerance levels.

Within CRE Construction Lending there are subcategories with their own specific risks to be considered; these should be thoroughly evaluated before an institution engages in any of these niche types of lending. We here explore several of these topics, and hope to assist in determining if Commercial Real Estate Construction Lending is an appropriate fit for your institution.

Today’s commercial lending environment has seen many regulatory changes, some of which specifically pertain to Construction Lending. Regulatory agencies now require institutions engaging in CRE Construction Lending to have performed a comprehensive and thorough review of an institution’s critical expertise in this area. This should be in conjunction with enhancements to the institution’s Credit Policy and a clear “Strategic Plan” before continuing or re- engaging in any Construction Lending. Additionally, reductions in the levels of CRE Construction/Renovation/Improvement loans as a percentage of capital and the loan portfolio have also been implemented.

The regulatory guidelines really set the stage for what a lender may or may not engage in, and should be the first element of the evaluation a lender should consider. The next element is the internal and external experience level of all the people involved in such projects in the past.

Questions that may assist in uncovering areas of concern internally may be:

- Was there an unrecognized lack of staff experience in this type of lending, causing inadequate underwriting and monitoring while problems were occurring?

- Were there documentation issues evident, including lack of Title Insurance, inadequate monitoring of liens filed, no updated title policy, or were weak covenants?

These issues may be evident by questioning, if there were underwriting weaknesses related to inadequate cash equity by a developer or sponsors at origination, or if the developers were not fully experienced with the type of project (size; cost; budget and timeframe).

When looking at the external expertise involved in these transactions some probing questions may be:

- Was an experienced engineering/inspection firm hired, or was this waived to save costs?

- Was the General Contractor (GC) adequate for the project (experienced as to type and scale of the project)?

- Was the GC replaced during construction and was the institution not immediately notified or notified well after the fact, with a replacement GC not approved and perhaps not as experienced? If so, why?

- What has been your institution’s prior experience in Construction or Renovation Lending?

- When and if losses were sustained, what were the reasons, and has the institution performed “post-mortems” to fully identify the reasons, including common threads or elements?

Analyzing the reasons for losses contributes to a stronger underwriting and improved monitoring when new projects are approved.

Diligent monitoring and reporting is an absolute necessity. After a lender has determined its appropriate regulatory guidelines, the expertise involved in past Construction Lending, and historical experience regarding losses, identifying the risk tolerance for these types of transactions should be addressed. Considerations include a tempered portfolio growth rate taking into account a lenders level of capital and its current loan portfolio mix, acceptable Loan to Value (LTV) limits, including supervisory limits, and Debt Service Coverage Ratios by type of property (which should be outlined in the current Credit Policies).

From a risk management standpoint, there should be periodic reporting to the board of directors, with updates on the various construction projects. Diligent monitoring and reporting is an absolute necessity to assure a successful project completion and then a subsequent performing loan. The basis of this monitoring would come from the Bank’s independent engineer’s ongoing status reports and validations for each construction draw request. If there are any problems which have developed they should be evaluated to determine their severity and their potential impact on the project. A reporting structure of this design assists the bank in protecting against a project not arriving at completion, which could play a part in a financial loss for the bank.

The three types of projects most often funded are: Apartment and Multifamily Projects

Apartment projects are perceived as lower risk, although there are still areas of concern to be evaluated and questioned specific to this type of lending. Always ensure that underwriting analysis determines whether a number of projects in the area are being started, either at the same time or separately: Could those projects be coming to completion at the same time, increasing the leasing risk and further potentially jeopardize the borrower’s DSC ability? What is the unit mix, the amenities, and the proximity is to local employers?

As with all Real Estate Construction projects, there should be pre- established minimum equity contributions, maximum LTVs based on value of the completed project, appropriate maturity commensurate with the size and scope of the project, a budget of total project costs, a plan and cost review by an independent construction consultant, an interest reserve appropriate for the duration of the loan, and a business plan demonstrating feasibility of the project.

Commercial (Office, Retail, and Industrial)

Included within this category could be anchored shopping centers or strip malls, hotel/motel facilities, regional tenant “standalone” facilities, or niche medical office facilities for doctors, dentists, surgical, or ambulatory centers. Condominium development and conversion projects have been the source of substantial credit losses for many regional banks over the past several years and as a result, little, if any, new projects are being introduced. The medical facilities, regional tenant standalone projects, shopping centers or strip malls and hotel/motel projects all require an in-depth understanding of the history of and current market direction of the affected local economies before any consideration can be made for funding in these areas.

The commercial environment throughout this country was severely affected by the recent recession, when many office buildings were erected on speculation or tenants were not financially strong enough to withstand the adverse effects of the economic downturn. There should be pre-existing leases from financially sound independent parties or a firm take-out commitment in place as requirements for any Commercial Construction Loan. As with any other type of Construction Lending, the Bank should investigate the character, expertise, and financial standing of all related parties. The developer, contractor, and subcontractors should be able to demonstrate the capacity to successfully complete the project. All final zonings should be in place for the intended use of the property prior to the first advance and bank’s credit policies regarding maximum LTV, minimum equity contribution, and the size and tenor of loan.

Participations

A participation (versus direct lending) in any of these projects can be an option when size of the project; expertise or risk appetite prevents fully funding such Construction Loans. Participations allow institutions to be involved in transactions, or pools of transactions that they otherwise would not be able to, because of regulatory and or geographical restraints. When considering participations, first evaluate your internal expertise in handling such arrangements.

The initial assessment of the lead institution on a participation arrangement should consider what the current expertise of that institution in this type of lending by asking:

- Does internal lending staff have the necessary expertise in handling these participation lending relationships?

- Does the bank have appropriate internal systems to track and monitor construction progress?

Even if the expertise is present, there must also always be open lines of communication between parties on these arrangements; at no time should there be an overreliance on the lead institution for administrating the loan. Participations can oftentimes become problematic when communication with the lead lender is not maintained throughout the project. It cannot be stressed sufficiently that the participant must remain fully informed and aware of all recent developments at each stage of construction.

Once the institution has determined its commitment to providing Construction Lending, recognizes its experience and expertise, identifies the type or types of projects it will finance, evaluates the many risks, determines the appropriate pricing against the risks in the loans, and establishes the necessary monitoring infrastructure and procedures, it could then proceed with the financing of such transactions. It is next imperative to engage an experienced real estate counsel who is aware of all conditions per approval of the Construction Loan; assignment of all contracts, permits, leases, etc.; all funding and draw requirements; and the guarantees required and pre-closing conditions pertaining to the project, borrower, and guarantors.

There are many considerations facing an institution when determining if Commercial Real Estate Construction Lending is an appropriate type of lending activity in the near future.