“Top Down” Capital Adequacy Assessment

The “Top Down” Capital Adequacy Assessment approach may be a suitable initial step to determine if further detailed analysis is necessary.

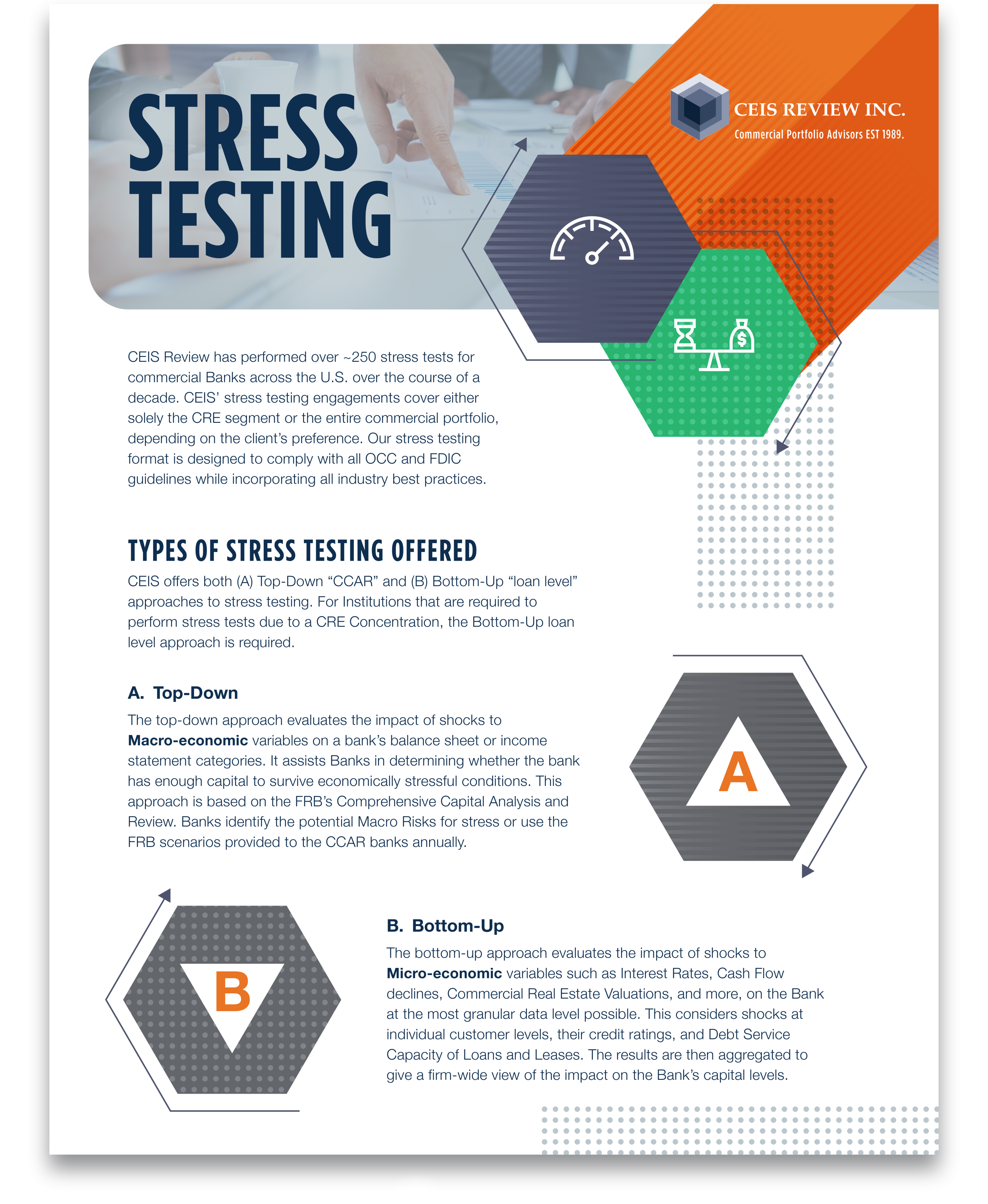

CEIS Review’s “top-down” approach is based on the Federal Reserve Bank’s Comprehensive Capital Analysis and Review (CCAR) model framework. It evaluates the impact of shocks to Macroeconomic variables on a bank’s balance sheet or income statement categories. It assists banks in determining whether they have sufficient capital to survive economically stressful conditions. Typically, Banks identify the potential Macro Risks for stress annually.

CEIS’ detailed and transparent analysis is the foundation of the engagement. We will segment the portfolio into pools with similar loss characteristics, develop “stressed” loss rates for each segment, calculate stress period loss amounts (minimum 2 year timeframe), estimate the earnings impact, and apply the earnings impact to Tier 1 Capital with both pre- and post-stress capital ratios.

Let’s schedule a call to learn more about out “Top Down” stress testing program.