I) The Operating Environment

The OCC (1) has observed overall increased bank earnings due to improved net interest margins, a strong quality and quantity of bank capital, and widely available liquidity. Credit quality remains strong, with all major loan categories reporting net charge-off rates below their 25-year averages. Interest rates and market volatility remain at or near historic lows. Regarding the unemployment rate, though wage gains are modest and inflation remains below target, the unemployment rate has declined below its pre-recession level. While conditions are positive in many aspects, regulators warn, as always, not to become complacent during times of prosperity.

II) Bank Performance

Net interest margins have reportedly increased for banks of all sizes, and net interest gains are the largest since 2010, ending a period of margin compression. For banks with total assets of $100mm-$500mm, as well as banks with assets $500mm-$1b, ROA is only 25%-33% below pre-crisis (1994-2006) averages. Contrastingly, among banks with less than $100mm total asset size, profitability is slower to recover; median pre-tax ROA is at about 60% of the pre-crisis average. The OCC believes that the divergence in profitability is driven by lower margins, slower loan growth, and higher operating costs relative to assets often experienced by small banks.

III) Trends in Key Risks: Asset Quality, Operational Risk, and Compliance Risk

Asset Quality Overview

“Asset quality remains strong, and overall underwriting is acceptable. Nonetheless, the credit

environment continues to be influenced by strong competition, tighter spreads, and slowing loan

growth. These factors are driving incremental easing in underwriting practices and increasing

concentrations in select loan portfolios—leading to heightened risk if the economy weakens or

markets tighten quickly.”

The thriving Commercial Real Estate market has been a driver of consistent growth in banks with total assets less than $1b. Banks with total assets greater than $10b experienced slower YoY growth in 2Q2017, due to a decline in Consumer and Residential mortgage loans, but maintained YoY growth in the Commercial & Industrial (C&I) and CRE loan segments. Below we will examine in further detail Asset Quality for major loan segments.

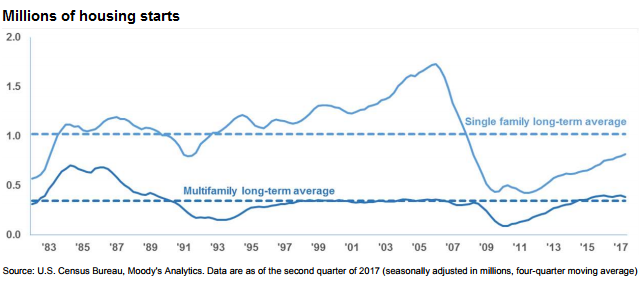

Housing construction is continually increasing and is weighted more toward Multifamily in comparison to historical averages. Specifically, the number of new Multifamily construction projects have historically averaged about 25% of housing construction projects, but comprised 32% of new housing projects over the last year. This increased focus on Multifamily construction is a direct response to declining homeownership rate among individuals between the ages of 20 and 34. Although Single-family projects continue to increase, they are still 20% below their historical average.

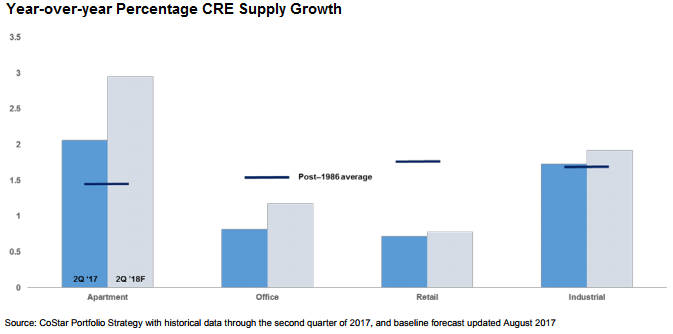

Multifamily growth remains strong, being the only property type with YoY growth significantly above its long-term average. As is presented in the chart below, Multifamily growth is notably stronger than growth in office, retail, or industrial property sectors.

Family residential home price appreciation continues in most states. Average home prices rose 6% YoY through 2Q2017, after increasing 5.4% the previous year. However, home prices remain below their peaks in the states that saw the greatest appreciation during the housing boom; home values in Nevada are >20% below their peak, and homes in Arizona, Florida, and Illinois remain >10% below peak values. Faster price growth overall has been nurtured by continued economic growth, low interest rates, and a limited supply of homes for sale.

Commercial loan growth experienced a remarkable expansion rate of 25% from 2014 – 2016, abating somewhat in the first half of 2017 but remains above GDP growth. Key drivers of this growth have been CRE lending and loans to a broad array of nondepository institutions, such as investment firms, mortgage companies, and finance companies.

Retail loan delinquencies remain relatively low but have increased from record low levels, particularly for auto loan and credit card exposures.

Overall delinquencies for Agricultural loans remain low, but are increasing. Due to lower agricultural commodity prices, farm cash income had been declining over the past three years, but is projected to modestly increase in 2017. Renewed declines in farm cash income could result in credit quality deterioration for banks with significant concentrations in agricultural lending.

Operational Risk

“Operational risk remains elevated as banks adapt business models, transform technology and

operating processes, and respond to increasing cybersecurity threats.”

The severity of cyber threats is increasing in both speed and sophistication. They target vulnerabilities that could, and have historically, exposed large quantities of personally identifiable information and proprietary intellectual property, as well as assisting in misappropriation of funds at the retail and wholesale level.

The use of third-party providers is increasing, and third-party risk management remains a supervisory focus. Additionally, increased use of a limited number of third-party service providers can create concentrated points of failure resulting in systemic risk to the financial services sector. Bank management is ultimately responsible for this, and can address these potential pitfalls through appropriate due diligence and ongoing oversight.

Being an independent third-party ourselves, CEIS Review has long been aware of the importance of testing the strength of our processes and controls. That is why we routinely commission an independent Service Organization Control (SOC) audit. This delves deeply into every aspect of our organization: Entity Level controls, Loan Review Processes, and Information Systems Environment elements; these elements include data security, logical access, physical security, environmental controls, data availability, and any changes to infrastructure. We have consistently been found to be exceedingly equipped in all aspects examined.

Compliance Risk

“Compliance risk remains elevated as banks continue to manage money laundering risks in an

increasingly complex risk environment. Implementing changes to policies and procedures to comply

with amended consumer protection requirements tests bank compliance risk and change

management processes.”

New technology and evolving criminal methods that support money laundering and terrorism-financing methods result in high Anti Money Laundering compliance risk (2). Though at the same time, evolving consumer tastes and expectations leave banks with little choice but to adapt. Understandably, many banks face difficulties validating banking processes and systems that are reliant on technology.

Since the Bank Secrecy Act (3) was established in 1970, and Anti-Money Laundering measures were established throughout the 80s and 90s, the level of technological sophistication that we have experienced creates a massive challenge to keep pace with evolving risks. New or amended consumer protection regulations such as the Truth in Lending Act (4), Real Estate Settlement Procedures Act (5) seek to address these evolving concerns. Consequently, ever changing regulation poses challenges for banks to adapt management processes, which increases operational, compliance, and reputation risk exposure.

IV) Supervisory Actions

Bank composite ratings (CAMEL scores) have improved, with ratings of 4 or 5 (meaning they are seriously or critically deficient at managing compliance risk) continuing to decline by 11% YoY. Enforcement Actions (EAs) against banks steadily continue to decline after peaking in 2009, reflecting an overall improvement in banks’ risk management practices and overall financial health. Matters Requiring Attention (MRAs) also continue to decline, as banks exercise sound governance, internal control, and risk management principles. As of June 30, 2017, top MRA categories of concern for large banks were compliance (36%), operational (35%), and credit (18%). Top risk areas of concern for community and midsize banks were operational (38%), credit (32%), and compliance (18%).

We here at CEIS understand the needs of community banks, and in our experience, have observed that the risks identified above – operational, credit, and compliance risk – are always on their mind. As the Loan Portfolio is typically the asset that presents the greatest potential risk for loss exposure to banks, Loan Review serves a very critical and essential function to the overall credit risk culture and controls of an Institution. If this function is left untended, not only could this possibly cause a change in the portfolios direction of risk, but it could also result in issues with the Institution’s auditors and regulatory bodies.

CEIS Review has been in business since 1989, and reviewing loan portfolios is what we do. At CEIS, we have established an unparalleled reputation that stands for expertise, efficiency, and integrity. We understand what it takes to work with all types of clients and the regulatory bodies that uphold legal and ethical standards. Every credit professional associated with CEIS has ~30+ years of lending and senior/executive experience that they bring to the engagement; you will gain the insight that the professionals bring, as well as feedback on industry best practices we observe in the market.

To learn more about how CEIS may assist your Institution, please contact us at [email protected] or by calling 888-967-7380.

Citations:

(1) https://www.occ.treas.gov/publications/publications-by-type/other-publications-reports/semiannual-risk-perspective/semiannual-risk-perspective-fall-2017.pdf

(2) http://www.finra.org/industry/aml

(3) https://www.occ.treas.gov/topics/compliance-bsa/bsa/index-bsa.html

(4) https://www.occ.treas.gov/topics/consumer-protection/truth-in-lending/index-truth-in-lending.html

(5) https://www.fdic.gov/regulations/compliance/respa/index.html